- 24/7 Free Consultation: (888) 424-5757 Tap Here To Call Us

How Long Does an Accident Stay on Your Record?

How long does an accident stay on your record is a common concern for many drivers after a crash. People often worry about how long a collision might affect their driving history, insurance rates, and financial health.

In Illinois, specific rules determine how long an accident remains visible on your record. Knowing these timelines and the factors that influence them can help you better prepare for the aftermath of a car accident.

Understanding Your Illinois Driving Record vs. Insurance History

Your Illinois driving record is maintained by the Secretary of State’s office. This official record keeps track of things related to the way you drive, including points from moving violations like speeding tickets, as well as reportable accidents.

A driving and accident record is mainly used for monitoring your status as a driver and determining if you have any infractions that might affect your license. When you get pulled over or apply for certain licensing, this record is what the state checks.

Insurance History and How It Differs

Car insurance companies maintain their own separate records to decide how much to charge for your policy and whether to offer coverage. These driving and insurance records go beyond just your traffic violations.

They include claims you’ve filed, accidents you were involved in, and other information gathered from sources like CLUE reports (Comprehensive Loss Underwriting Exchange), which compile insurance claim data from multiple insurance carriers.

Your insurance history helps companies assess risk and set your premiums, but it doesn’t necessarily correlate exactly with what the state’s driving record reflects.

Why the Difference Matters

Because the driving and insurance records contain different types of information and serve different purposes, an accident or violation might influence each differently.

An accident could stay on your record for a certain period but remain on insurance reports longer, potentially keeping insurance company premiums higher even after it no longer appears on your driving history. Knowing this distinction helps you understand what impact an accident might have.

When Must a Car Accident Be Reported in Illinois?

In Illinois, you must report that an accident occurs if it involves an injury, fatality, or property damage over $1,500. If a driver is uninsured, the threshold drops to $500. Under 625 ILCS 5/11-408, police typically report accidents they handle to the Illinois Secretary of State.

However, if no police report is filed, drivers must submit a written report within 10 days. Failure to comply can lead to fines and penalties.

Do Car Insurance Companies Report Accidents to the State?

Car insurance companies generally do not report individual accidents to the Illinois DMV or Secretary of State. Instead, reporting is the responsibility of the police and drivers, who must notify the state when required.

However, insurers may notify authorities about policy changes, cancellations, or the need for an SR-22 certificate, which proves you have the required insurance after specific violations. Knowing these processes helps you understand how accidents and insurance impact your DMV record and legal standing in Illinois.

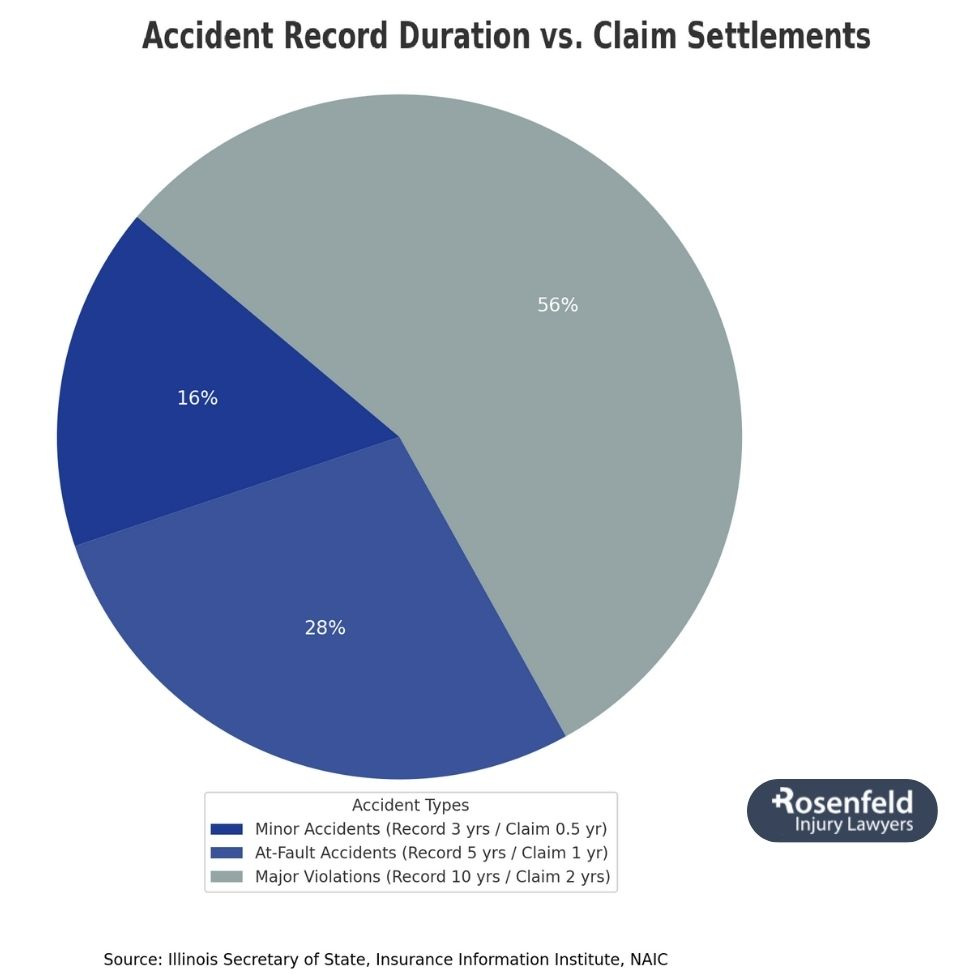

Typical Duration: How Long Will an Accident Stay on Your Record for Car Insurance Purposes?

For most insurance companies, most accidents will impact your car insurance rates for about three to five years after the incident. This timeframe marks how long insurers typically review your accident history when deciding your premiums and eligibility.

After this period, many insurance companies stop considering that accident in their risk assessments, which can help lower your insurance costs. While exact timing can vary between companies, three to five years is the common window during which the accident remains relevant for insurance purposes.

How an At-Fault Accident Impacts Car Insurance Premiums

If you’re found at fault in a car accident, it’s common for your car insurance premiums to rise when it’s time for the company to renew and calculate premiums. On average, car insurance rates can climb significantly. Some studies show that drivers may see increases of around 45% nationwide after an at-fault crash.

Car insurance companies view these accidents as indicators of higher risk, so they adjust premiums accordingly to reflect that increased chance of future claims.

Factors Influencing Your Car Insurance Rate Increase

Several factors play a role in determining how much your car insurance rates might rise after an at-fault accident. These can include:

- How serious the accident was, including the cost of property damage and injuries

- Your driving history, especially whether you’ve had a clean accident record or multiple incidents before

- Whether you were cited for any traffic violations connected to the crash, like speeding or running a red light

These elements help insurers assess risk and decide how to adjust your premiums.

Will a Not-At-Fault Accident Affect My Illinois Insurance Rate?

In Illinois, where the at-fault driver’s insurance is typically responsible for covering damages, a no-fault accident usually shouldn’t cause a major increase in your car insurance premiums.

Because you weren’t the driver responsible for the crash, most companies won’t raise your insurance rates the same way they would if you were at fault. However, some insurers might still adjust premiums slightly after a no-fault claim, although these changes tend to be smaller and less frequent.

How Long Do Higher Insurance Rates Typically Last?

When an auto insurance company raises your insurance rates because of a car accident, those higher premiums usually stick around for about three to five years. Over time, if you avoid any additional tickets or claims and keep a clean record, the extra surcharge related to the accident should gradually go away.

Eventually, your insurance costs can return to normal, rewarding you for safe driving following the incident.

Impact of Serious Violations (DUI, Hit-and-Run) on Your Record

Certain serious violations, like drunk driving (DUI conviction), reckless driving, or leaving the scene of an accident, leave a lasting mark on your DMV record. Unlike minor traffic offenses, these serious charges often stay on your record for much longer, sometimes a decade or even indefinitely.

Because car insurance companies see these violations as signs of significant risk, they can lead to much higher premiums or difficulty finding coverage. The long-term impact serves as a strong reminder to maintain safe driving habits to avoid these costly consequences.

What is Accident Forgiveness Coverage?

Accident forgiveness is a feature that some insurance companies offer, either as part of your insurance policy or as a reward for safe driving over time. It means your insurer, like Allstate or Liberty Mutual, for example, won’t increase your premium after your first accident, even at-fault accidents.

However, it’s important to understand that while single accident forgiveness may prevent an insurance rate hike with your current company, it doesn’t remove the accident from your DMV record or from reports that other insurers might see. This coverage can provide some financial relief, but it’s not a guarantee that all future auto insurance providers will ignore the car accident.

Strategies for Lowering Car Insurance Premiums After an Accident

After a car accident, it’s natural to worry about your driving future and higher insurance premiums, but there are several steps drivers can take to reduce those increases and save money over time.

Utilizing Defensive Driving Courses for Potential Discounts

One way to possibly lower premiums is by taking a state-approved defensive driving course. Many insurers offer discounts once you complete these programs. Before enrolling, it’s a good idea to check with your auto insurance company to make sure they recognize the course and to find out what kind of savings you might qualify for.

Improving Driving Habits and Using Telematics Programs

Another option is to enroll in telematics or usage-based insurance programs. These track your driving habits, including how smoothly you brake, accelerate, the times when you drive, and how many miles you cover. Consistently safe driving recorded through these programs can lead to discounts, which might help offset any increases caused by a car accident.

Other Ways to Save (Discounts, Deductibles, Credit Score)

Beyond these, there are other ways to cut costs on your insurance. Always ask your insurer about all available discounts, such as bundling multiple policies, having more safety features installed, or good student incentives.

Consider choosing a higher deductible to lower your premium, but be mindful that this means paying more out of pocket if you have another claim. Improving your credit score over time can also have a positive effect, as many insurers use credit information to set insurance product prices in states that allow it.

By combining these strategies, you can better manage your insurance expenses while continuing to drive safely and responsibly.

The Importance of Maintaining Safe Driving Practices Post-Accident

After a car accident, the most effective way to lower your insurance premiums once the surcharge period ends is by learning driving skills and by driving safely. Consistently following traffic laws and avoiding new tickets or crashes shows insurers that you’re less of a risk, which can help reduce your rates over time.

Can Car Accidents Be Removed From Illinois Driving Records?

In Illinois, mistakes on your driving record can sometimes be corrected or removed, but it’s rare for motor vehicle accidents to be taken off if they were properly reported. Accidents where no fault was assigned or incidents that didn’t meet the minimum reporting requirements might not even show up on your record.

However, once a car accident is accurately recorded by the state, it usually remains there for a while. This means most accurate motor vehicle accident entries remain part of your official history until the period expires, so it can take a bit of time before you have a clean driving record again.

How to Check Your Own Illinois Driving Record

If you want to see your official driving record in Illinois, you can request it directly from the Secretary of State’s office. You have several options to get a copy: you can order it online through their website, send a written request by mail, or visit a local Secretary of State facility in person to obtain it.

Checking your record regularly helps you stay informed about your driving history and verify that all information is accurate.

Handling Non-Renewal or High-Risk Insurance Needs

If you’ve had multiple motor vehicle accidents or serious driving violations, your car insurance company may decide not to renew your insurance policy.

This can make it challenging to find insurance coverage on the open market. In these cases, drivers can turn to the high-risk insurance pool, also known as the assigned risk program, which provides a way to maintain the required coverage.

While policies in this market tend to be more expensive, they offer an important option for drivers who have trouble getting insured elsewhere.

Role of Legal Support in the Underlying Accident Claim

While this article focuses on how accidents affect your driving record and auto insurance rates, it’s important to remember that legal help plays a vital role in the actual injury claim itself.

- A knowledgeable car accident lawyer can help establish who was at fault for the crash.

- They assist in addressing the medical and personal finance challenges that come with injuries from a motor vehicle accident.

- An attorney works to negotiate with the responsible parties or car insurance companies to secure fair compensation for your losses.

- They guide you through the legal process and protect your rights.

Having strong legal support is essential to effectively handle the injury claim and pursue the full financial recovery you deserve.

FAQs About Illinois Driving Records & Car Accidents

Do Points Associated With a Car Accident Stay on My Illinois Record Indefinitely?

Points from traffic violations linked to a motor vehicle accident do not remain on your Illinois driving record forever. Typically, these points stay for a few years, usually around two to three years, but up to five years, depending on the type of driving violation. After that, they may be removed, helping to clean up your record over time.

However, the accident itself, especially if it involved a reportable crash, can stay on your record for a longer period.

How Many Points Typically Lead to a Driver’s License Suspension in Illinois?

In Illinois, your driver’s license can be suspended or revoked based on how many points you accumulate from traffic violations.

For drivers 21 and older, reaching 15 to 44 points often leads to a two-month suspension, while accumulating 110 or more points typically results in license revocation. The length of suspension increases with more points, ranging from two months up to a year.

Additionally, some serious offenses can lead to immediate suspension or revocation regardless of your point total. If you commit multiple violations in a short time, the state may take action against your driving privileges.

Can Taking Defensive Driving Courses in Illinois Remove Points From My Record?

In Illinois, defensive driving courses generally don’t remove points that are already on your driving record. However, attending a driver safety program can sometimes stop points from being added in the first place.

When you get a ticket, like a speeding ticket, for example, you might have the option to pay the fine and take a traffic school course to prevent the violation from showing up on your driving and insurance record, but this option is limited to a certain number of times within a year. If you can’t go to traffic school or don’t qualify, you may have points added to your record.

If I Pay for Damages Out-of-Pocket and Don’t File an Insurance Claim, Will the Accident Avoid My Record Entirely?

Paying for damages yourself might prevent an insurance claim from being filed, but it doesn’t necessarily mean the accident won’t appear on your official driving record. Accidents that meet Illinois reporting thresholds, such as those involving significant property damage or injury, are often required to be reported to the state regardless of insurance involvement.

According to the Insurance Information Institute, an accident reported to insurance or if a police report is created could cause your rates to increase.

Additionally, the other party involved with the claim may report the accident to their insurance company. So, even if you don’t report it to your own insurance company, they may still find out about the accident, even if you pay out of pocket.

Protecting Your Driving Record and Future Insurance Rates

Your driving record and car insurance rates can have a big impact on your daily life and personal finances. Our car accident law firm in Chicago is here to support you through every step, providing experienced guidance to help you safeguard your driving and insurance records and fight for fair compensation if you’ve been injured.

If you have questions or need assistance, don’t hesitate to contact us for a free consultation. Call (888) 424-5757 or complete our online contact form.

All content undergoes thorough legal review by experienced attorneys, including Jonathan Rosenfeld. With 25 years of experience in personal injury law and over 100 years of combined legal expertise within our team, we ensure that every article is legally accurate, compliant, and reflects current legal standards.